Modern life lending solutions.

Plan and protect for a better retirement.

Glenn Issler. Mortgage Advisor.

Serving British Columbia & Alberta

Planning your mortgage and finances through retirement can be frustrating. It doesn't have to be when you follow my 3 step plan.

Connect with me

Contact me to schedule an initial consultation. We'll discuss your financial goals and unique needs, laying the groundwork for a tailored plan.

Put together a Plan

Together, we'll create a customized retirement plan using modern life lending solutions, maximizing your financial security and peace of mind.

Proceed with confidence

With a solid plan in place, you can confidently navigate your retirement journey, knowing you're well-prepared for a comfortable and fulfilling future.

Providing mortgage solutions for employees, retirees, and small business owners.

Hello, I'm Glenn Issler, a dedicated Canadian mortgage advisor with a passion for helping clients aged 55 and over find the perfect financial and mortgage solutions to plan for a comfortable retirement. With years of experience and a keen understanding of the unique needs of employees, retirees, and small business owners, I'm committed to providing you with modern life lending solutions tailored to your individual circumstances.

My approach is a seamless blend of professionalism, respect, and a genuine desire to see my clients succeed. I believe that by fostering a polite and inviting atmosphere, we can work together to explore the options available to you and create a plan that truly aligns with your retirement goals. Whether you are an employee, retiree, or a small business owner, I am here to guide you every step of the way.

I encourage you to connect with me directly so we can discuss how I can help you achieve the retirement you deserve. Together, let's make your financial dreams a reality. Please don't hesitate to reach out, and I look forward to working with you on your journey towards a better retirement.

Nice things people have said about working with me.

Nice things people have said about working with me.

Are You Over 55?

I'd love to gift you this book.

In this accessible and informative book, HomeEquity Bank CEO Steven Ranson and Executive Vice President Yvonne Ziomecki delve into the intricacies of reverse mortgages. Discover how these financial tools can offer Canadians aged 55 and above a pathway to a secure and fulfilling retirement.

Contact Us

We will get back to you as soon as possible.

Please try again later.

Are You Over 55?

I'd love to gift you this book.

In this accessible and informative book, HomeEquity Bank CEO Steven Ranson and Executive Vice President Yvonne Ziomecki delve into the intricacies of reverse mortgages. Discover how these financial tools can offer Canadians aged 55 and above a pathway to a secure and fulfilling retirement.

Contact Us

We will get back to you as soon as possible.

Please try again later.

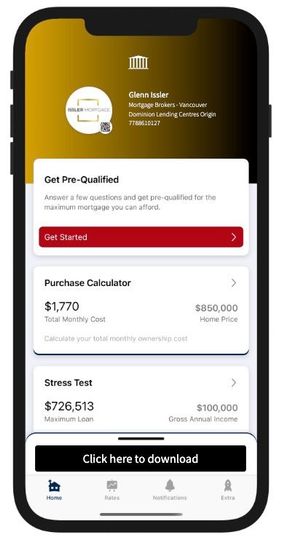

Download my Mortgage Toolbox App

What you can do with my app

Calculate your total cost of owning a home

Estimate the minimum down payment you need

Calculate Land transfer taxes and the available rebates

Calculate the maximum loan you can borrow

Stress test your mortgage

Estimate your Closing costs

Compare your options side by side

Search for the best mortgage rates

Email Summary reports (PDF)

Use my app in English, French, Spanish, Hindi, and Chinese

Mortgage financing for Canadians planning into their retirement.

Financial Peace of Mind: Building the foundation for your well-deserved retirement

Mortgage articles to keep you informed.

Get started by completing my online mortgage application.

I'll let you know exactly where you stand so you can proceed with confidence.